Home

Home Saral Gyan Freebies

Saral Gyan Freebies Saral Gyan Services

Saral Gyan Services About Us

About Us Contact Us

Contact Us

Value investor Warren Buffett also falls in the inefficiency camp, claiming that individual investors should be able to earn 50% annual returns with small amounts of money because they have access to high-return small-cap stocks that he can no longer buy because of Berkshire’s huge asset size

Facts about Small Cap Companies

1.If you want out sized returns, you must invest in small-cap value stocks.

2.All ten of the top-performing stocks of the past decade were small caps and most were value stocks. We can almost guarantee that the top-performing stocks of the next decade will be small caps as well.

3.Most small caps under perform, so the key is either finding the few small caps that will produce the 30, 40, and 50-baggers, or instead buying the entire small-cap universe to insure that you won’t miss out on the big winners.

4.Small caps have above-average volatility and can under perform for long periods, so their out sized returns may require a long time frame to be realized.

5.Whether small caps are inherently more risky or just inefficiently priced is undecided, but investment prudence dictates that you normally limit your small cap allocation to less than half (some say 35%) of your total equity portfolio and avoid them altogether during incipient periods of severe economic distress.

For a stock market investor, it is financial information of the company which guides him whether he should buy or sell the company’s stock. For a micro cap stock, this information is sometimes not available since some micro cap companies do not even file their financial reports to stock exchanges. Therefore, it is hard to evaluate a micro cap company using normal technical analysis methods.

What is a micro cap stock?

A micro cap company is a company having low or micro market capitalization. The term micro-cap stock (also micro-cap) is used to describe publicly traded companies which have a market capitalization of roughly Rs. 500 crore or less. Micro cap stocks are usually not able to satisfy the eligibility criteria of being listed on major exchanges.

Micro-cap companies are known for their volatility and many such companies are involved in fraud. Since the institutional investors are rarely involved in these stocks, the stock price can be manipulated by the investors. Even though these stocks come in high risk category, investors can’t turn their eyes away from them since these can be highly profitable as well. These stocks have given higher returns than large cap stocks since last 10 years. This is the reason there are a few indices specially track the performance of micro cap stocks globally. Some of these indices are Russell Micro-cap Index, the Dow Jones Select Micro-cap Indexes, and the Dow Jones Wilshire U.S. Micro-Cap Index.

In India, BSE Small Cap Index is a well known index. BSE Small Cap Index is a composition of 865 companies. Its good to point out that most of the fortune investors invested in small/micro cap stocks in early stage of their lives, hence a small pie of your portfolio could be of small / micro cap stocks, which can have the potential to change your fortune in years to come by turning to true multibaggers creating enormous wealth.

Grow your Wealth by Investing in Hidden Gems Now!

Its a fact that 50 small and micro cap stocks out of 87 recommended by our team under Hidden Gems service during last 9 years have given more than 100% returns. Stocks like Cera Sanitaryware, Camlin Fine Sciences, Kovai Medical, Wim Plast, TCPL Packaging, Mayur Uniquoter, Roto Pumps etc are our multibagger stocks have given whopping returns in the range of 400% to 2000%.

Below are some of the Hidden Gems stocks released by us which turned out be multibaggers during last 9 years. Even after severe correction in small caps over last 1.5 years, as on date returns is in the range of 150% to 1800%. In fact, we already advised partial / full profit booking in many of these stocks at higher levels. The update of the same was published in our Hidden Gems Flash Back report.

HIDDEN GEMS STOCKS

|

RELEASE DATE

|

MULTIBAGGER

|

OLD REPORT

|

|---|---|---|---|

| 1. Camlin Fine Sciences |

27 Mar 2011

|

8-BAGGER

| |

| 2. Wim Plast |

30 Aug 2011

|

5-BAGGER

| |

| 3. Kovai Medical |

27 Oct 2011

|

7-BAGGER

| |

| 4. Cera Sanitaryware |

24 Dec 2011

|

19-BAGGER

| |

| 5. Mayur Uniquoter |

31 Mar 2012

|

5-BAGGER

| |

| 6. Roto Pumps |

05 Aug 2012

|

7-BAGGER

| |

| 7. Acrysil |

25 Nov 2012

|

5-BAGGER

| |

| 8. TCPL Packaging |

31 Mar 2013

|

5-BAGGER

| |

| 9. Rane Brake Lining |

31 May 2014

|

3-BAGGER

| |

| 10. Dynemic Products |

29 Jul 2014

|

2.5-BAGGER

| |

| 11. Mold-Tek Packaging |

22 Mar 2015

|

2.5-BAGGER

| |

| 12. Visaka Industries |

05 Jul 2015

|

3-BAGGER

| |

| 13. Chemfab Alkalies |

06 Sep 2015

|

2.5-BAGGER

| |

| 14. Ultramarine Pi. |

11 Oct 2015

|

2.5-BAGGER

| |

| 15. Stylam Industries |

08 May 2016

|

3-BAGGER

|

Post election outcome, Sensex & Nifty made all time high and delivered positive returns of ~15% since Jan 2018 where as broader markets i.e. Small Cap and Mid Cap indices delivered negative returns of 29% and 20% respectively during the same period. Most of the liquidity in small & mid caps has dried up and found its way to large caps over last 1.5 years. At this juncture, large caps looks fairly valued or expensive in terms of valuations, however small & mid cap companies look attractive and can reward long term investors in big way. In fact, some of the worst times to get into the market turned out to be the best times for long term investors and same seems to be applicable now for small & mid caps.

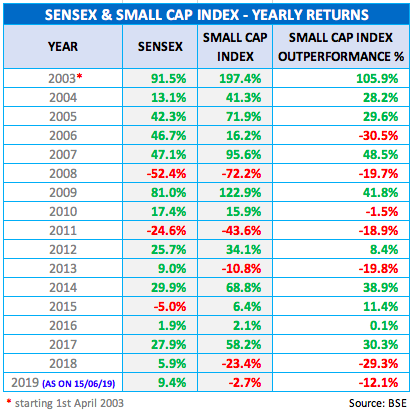

Small Cap Index has not delivered negative returns for 2 consecutive years in past 16 years

We believe this is a blessing in disguise because for the first time in many years, several small companies having robust business fundamentals are available at attractive valuations. Do you know in last 16 years, small cap index have not given negative returns for 2 consecutive years. In 2018, BSE Small Cap Index has given negative returns of -23.4% and since beginning of this year, index is down by another -4.4%. Below is the table which indicates Small Cap Index returns YoY since 1st April 2003 (the data is available from April 2003 onwards only in BSE).

Whenever, Small Cap Index delivered significantly high negative returns in a particular year during last 16 years, it has delivered double digit positive returns the very next year. The divergence between Sensex / Nifty and Small & Mid Cap Index will not last for long going forward considering valuations gap emerging between large caps in comparison to mid & small cap stocks.

Whenever, Small Cap Index delivered significantly high negative returns in a particular year during last 16 years, it has delivered double digit positive returns the very next year. The divergence between Sensex / Nifty and Small & Mid Cap Index will not last for long going forward considering valuations gap emerging between large caps in comparison to mid & small cap stocks.

Tide to turn favourable sooner than later for small cap stocks

If you analyse the bear phase of stock markets cycle since 1990, you will find that such bear phase has not lasted for more than 18 months. Small cap index which made high in Jan 2018 with end of its bull run corrected by -35% from its peak of 20,184 in Feb 2019 and we believe bottom in broader markets is already in place with lows made in Feb 2019 post Pulwama attack.

Be a disciplined investor who keep on investing in systematic way irrespective of market conditions and not an emotional investor who usually buy stocks during bull phase when stock prices are moving higher because of greed and sell them in panic during bear phase due to severe fall in stock prices, making mistake of buying high and selling low.

Greed which was seen in broader market (small & mid caps) in the year 2016 and 2017 has turned to fear these days. Are you also fearful? This is the time to do opposite of the herd, its time to be greedy when others are fearful. If you are not investing in equities during these opportune times and taking the back seat, you are making a bigger mistake.

Remember, in the long run, you do not make decent returns on your investments by following the herd i.e. when everyone is buying stocks; instead you get handsome returns on our investments by investing in stocks at significantly low prices as no one else is buying, and by selling to them when they come back in herd due to greed in future.

Remember, in the long run, you do not make decent returns on your investments by following the herd i.e. when everyone is buying stocks; instead you get handsome returns on our investments by investing in stocks at significantly low prices as no one else is buying, and by selling to them when they come back in herd due to greed in future.

Be a disciplined investor who keep on investing in systematic way irrespective of market conditions and not an emotional investor who usually buy stocks during bull phase when stock prices are moving higher because of greed and sell them in panic during bear phase due to severe fall in stock prices, making mistake of buying high and selling low.